Highway to Financial Freedom

- Subham Sahu

- Jul 23, 2017

- 5 min read

Why do you earn? Why do you need money?

To buy that dashing Harley, or

To go on a Europe tour, or

To buy that sea facing villa (Goa or Pondy?), or

To buy that Jet, or

To have a better lifestyle, or

To earn the freedom of leaving your job at your choice, or

To improve the lives of your dependents (may be that slum kid you always wanted to help)

If we try to find the answer to why money is important in our life, we will notice one very significant thread: we need money to earn our freedom. Actual freedom is to fly at our own wish, freedom to choose our work, freedom to travel without a thought of what will happen if I don’t turn up in office on Monday. If you have sufficient money to buy an iPhone, you have the freedom to choose between iPhone and anyPhone. However, what if you can’t afford an iPhone? Congratulations for your new anyPhone. Money is that little freedom more than anything else.

Remember this quote from one of the richest actors

Photo Credit: IndiaToday

Money is important. But the question is how to create wealth? How to earn money? (Note that money and wealth are not the same thing. We will discuss “difference between Money and Wealth” and “ways of creating wealth” separately).

For this article it is assumed you have a steady income source, either as an employee of an organisation or running your own business or freelancing.

Since you have a steady income, what should you do now? Buy a new KTM on EMI? Savings? Investing?

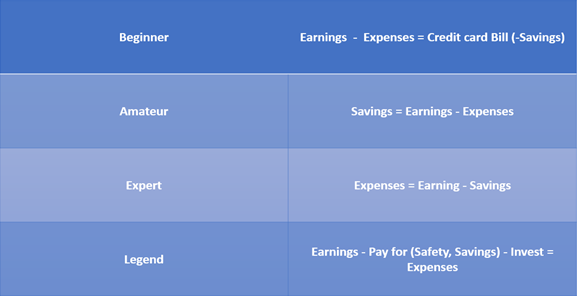

Normally, we spend from what we earn and save the rest. Thereby we have set expenses as our priority. Since the priority is “expenses” over “savings”, we have to face what is called ‘paycheck to paycheck living’. And the basic problem with this approach is we don’t consider economic uncertainty, the probability that your earning may vanish, or that a new need may arise.

When you are planning for a home, family, children’s education or even your Euro trip, one of the problems is the money you need, but don’t have. So let’s start on how to plan your budget considering all the aspects of life: uncertainty, goal achievement, and creating wealth (thereby increasing the quality of life).

The priority for allocation of capital (your hard earned money) should be managing your risks, saving to achieve your goals, and then growing your capital.

We will discuss each step subsequently.

First Pay for Safety : Risk Management

[if !supportLists]● [endif]Buy a Term Insurance : Insure your death

“Like death of my dearest son was not enough, we are now blessed with poverty too. With his death, his son’s dreams are also on the verge of being buried.” cried the mother of late Mr. Singh.

Many lives are dependent on us. Our earnings are bread and hope for all our dependants. So, we should plan to make their lives less painful and ensure that the cash inflow is not discontinued. So, buying a Term Insurance would be a good strategy. A plain vanilla “Term Insurance”. Don’t expect anything other than the financial security of your dear ones. They are cheap and you can buy them online directly. Online plans are 30-40% cheaper than your insurance agent due to lower distribution cost for company.

Approximate cost of term insurance for a sum of 1 Crore is Rs.1000/- per month for someone in their 20’s and the cost increases with age.

[if !supportLists]● [endif]Buy Family Health Insurance : Insure the greatest wealth i.e. you and your family’s health

With innovation and advancement, we are able to find new ways of living longer and healthier life. But that comes at a cost. Are we able to pay for ever increasing healthcare costs? Can we pay for any critical illness that may arise? So, buy a health insurance.

Last but not the least, safety aspect of personal finance is not only buying Insurance, it’s about buying safety so that you can have a healthy and wealthy life. For example, we suggest buying a car with better safety features even if it costs more. Do buy other insurances where you see there can be economic ramifications.

To know more about this, mail us.

Instruments for Risk Management: Insurance, Investment for buying safer things (like buying airbags while buying a car), etc.

Second Save for now and future : Goal Achievement

[if !supportLists]● [endif]Save for the turbulent times

It’s inevitable that economic situations change and therefore your ability to earn. Your loss of job or business may lead to days where you will be bound to take debt. However remember that bankers don’t like to have poor clients. Bank offers you loan when they see your financial ability to repay is high but not otherwise.

So, put a sum of money in a liquid fund which you can access anytime. Do not touch this fund unless it’s very urgent. As a thumb rule, sum of the money for this kitty should be “estimated monthly expenses for six month ”

[if !supportLists]● [endif]Follow a goal based saving plan

Can you recall the words “EMI” and “Credit Card”, which are sold by bankers as a panacea for your deficiency of shopping power? You know the banker prays that you miss the payment of EMI and he/she can charge you 30-40% interest. Yeah, your lovely Euro trip won’t be as lovely as you had expected if you buy using EMI.

So, follow reverse-EMI. Save some part of your earning as a recurring deposit for that specific purpose. Have different accounts for your Harley and Euro Trip.

Each goal based fund/account should typically be for 1-3 Years.

(To those who think they will lose the benefit or discounts offered by “Credit Cards”, believe me there are other ways of availing the benefit.)

[if !supportLists]● [endif]Save for future : Long term

Save for your future. This should be the fund which you are saving for your needs of next five years. This fund is for every big need that will arise, like to buy your house, or for marriage, or for children’s education.

Instruments for Saving : RD, FD, Short-Term Liquid Mutual Funds etc.

Finally Invest : Capital growth by compounding

Investing is for creating wealth in future using present wealth. At present you have time, health, money and other assets. But how should you use these assets to create future wealth? Lets explore...

[if !supportLists]● [endif]Invest on yourself

Investing in You, and Your Skillset should be the priority.

“You” means your health, physical and Mental. Buying your gym membership is investing on you. Paying more to eat better food is investing on you. Similarly, find ways to invest for a better You.

Your skillset gives you the earning capability and associated dignity. So invest in buying books and going for conferences. Investing in your learning will give you a better earning capability.

In short, Invest in sharpening your saw, returns will be exponential.

[if !supportLists]● [endif]Invest for exponential capital growth

What’s your plan for your children’s education with ever increasing college fees? What’s your plan for retirement? Without your paycheck, how will you maintain your lifestyle? Are you sure your savings will suffice?

Such requirements need special attention i.e. something more than savings. You need capital multiplier and the tool for this is compounding.

“Compound interest is the eighth wonder of the world. He who understands it, earns it ... he who doesn't ... pays it. Compound interest is the most powerful force in the universe.” - Albert Einstein

Remember this line from Mr. Einstein. invest for your future. Take advantage of compounding. In the long term the risk of such investments are almost zero.

Instruments of Investing : Physical Assets (like land or real estate), mutual funds, bonds, equity (shares), gold, ETFs

Risk is associated with all kind of Instruments (Mutual Fund, Equity etc). In some there is high risk and in some it’s low. While investing in any instrument,, learn the risk associated with it. We will publish an article on risk appetite and risk association in coming weeks.

Comments